Commerce Exam > Commerce Notes > Accountancy Class 11 > Short Notes: Theory Base of Accounting

Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce PDF Download

Introduction

- Accounting information must be reliable (accurate, trustworthy) and comparable (enables pattern/trend analysis) for internal and external users.

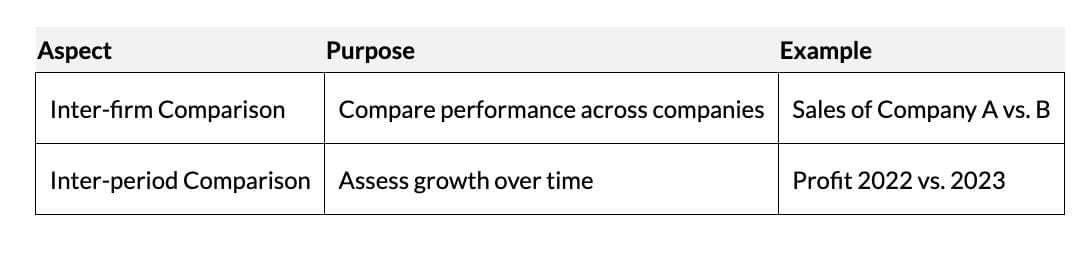

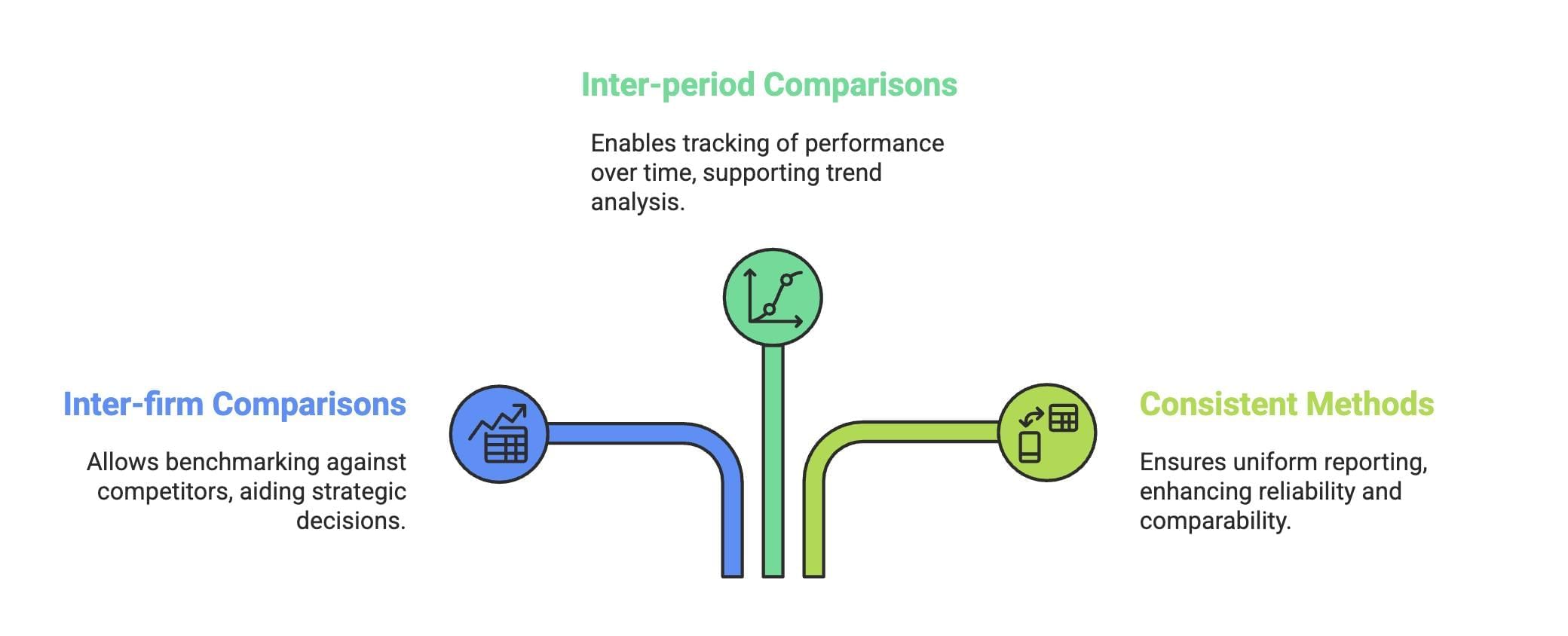

- Comparability: Facilitates better decision-making through inter-firm and inter-period comparisons:

- Consistency: Using the same accounting methods over time ensures meaningful comparisons across firms and periods.

Accounting Process and Consistency

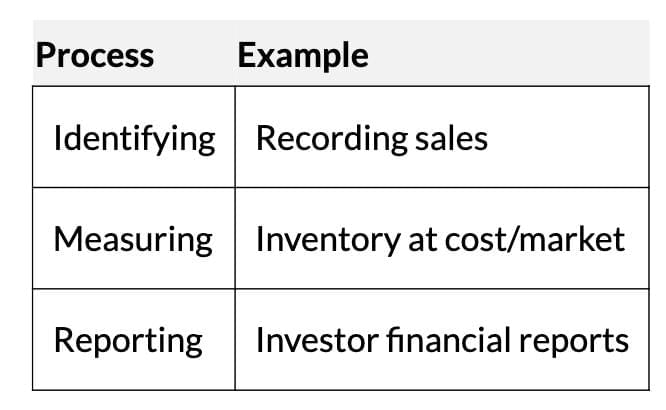

Consistency in accounting involves uniform methods in:- Identifying transactions (e.g., sales, expenses).

- Measuring transactions (e.g., valuing inventory at the lower of cost or market price).

- Recording in books of accounts (e.g., income, assets).

- Summarising results (e.g., financial statements).

- Reporting to stakeholders (e.g., investors).

Consistency ensures reliable financial statements for decision-making.

Theory Base of Accounting

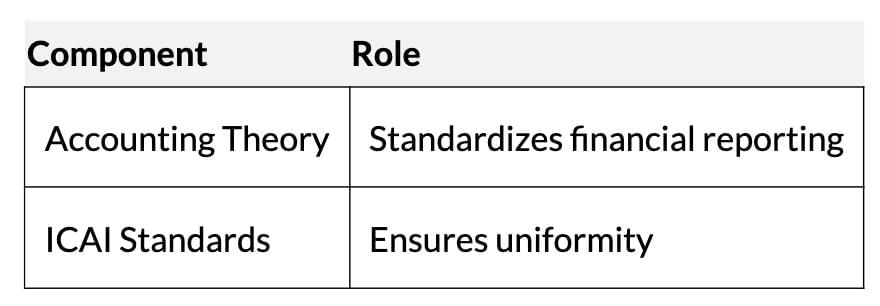

- Accounting theory provides a standard framework for recording, measuring, and reporting financial information.

- Comprises principles, concepts, rules, and guidelines for consistency and uniformity.

- The Institute of Chartered Accountants of India (ICAI) sets Accounting Standards to ensure uniform practices.

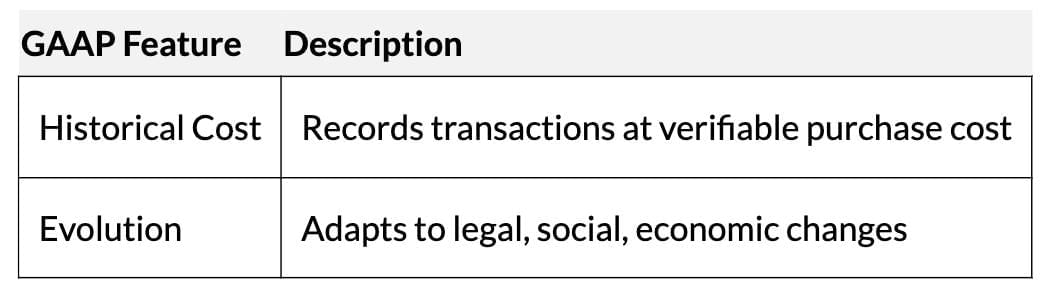

Generally Accepted Accounting Principles (GAAP)

- GAAP are rules for the consistent recording and reporting of business activities.

- Include principles, concepts, conventions, postulates, and assumptions, often used interchangeably.

- Evolve based on experience, professional standards, and legal/economic changes.

- Example: Recording transactions at historical cost (e.g., using cash receipts) enhances objectivity.

Basic Accounting Concepts

Fundamental assumptions guiding accounting practices:- Business Entity: Business is separate from owner; e.g., owner’s ₹1,00,000 investment recorded as capital.

- Money Measurement: Only monetary transactions recorded; e.g., land valued at ₹2 crore, not physical size.

- Going Concern: Assumes business continues indefinitely; e.g., computer cost (₹50,000) depreciated over 5 years.

- Accounting Period: Financial statements are prepared for specific periods, typically annually.

- Cost: Assets recorded at purchase cost; e.g., plant recorded at ₹50,50,000 including transport/installation.

- Dual Aspect: Every transaction affects two accounts; e.g., ₹50,00,000 investment increases cash and capital.

- Revenue Recognition: Revenue is recorded when earned; e.g., construction contract revenue is recognised proportionately.

- Matching: Expenses matched with revenues; e.g., cost of goods sold matched with sales revenue.

- Full Disclosure: All material facts disclosed; e.g., SEBI mandates complete financial disclosures.

- Consistency: Uniform accounting methods over time; e.g., same depreciation method yearly.

- Conservatism: Record losses, not unrealised gains; e.g., stock valued at the lower of cost/market.

- Materiality: Focus on significant facts; e.g., theatre upgrades disclosed as material.

- Objectivity: Transactions backed by verifiable evidence; e.g., machine purchase recorded via receipt.

Systems of Accounting

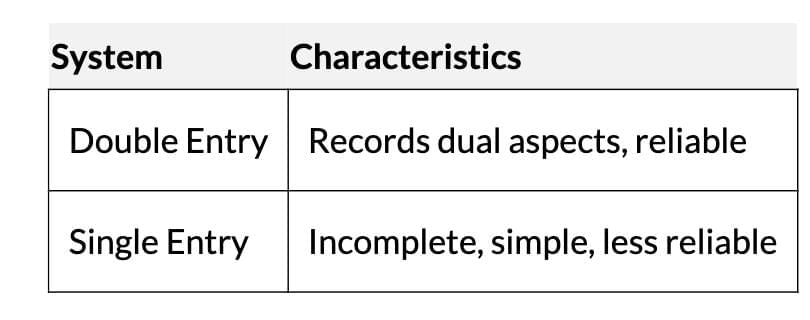

Double Entry System:- Based on Dual Aspect, every transaction affects two accounts (debit/credit).

- Complete, accurate, reduces fraud; e.g., trial balance checks errors.

- Used by large and small organisations.

- Incomplete, records only one transaction aspect; e.g., only personal accounts/cash book.

- Simple but unreliable, used by small businesses.

Basis of Accounting

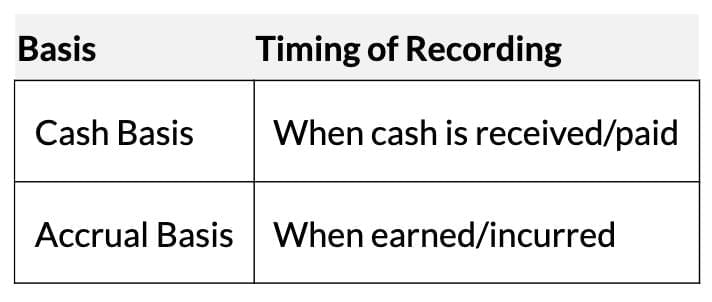

Cash Basis:- Records transactions when cash is received/paid; e.g., December 2014 rent recorded in January 2015.

- Incompatible with the matching principle, less accurate for profit calculation.

- Records revenues/costs when earned/incurred, not when cash is exchanged.

- Aligns with the matching principle; e.g., raw materials consumed matched with sales revenue.

Accounting Standards

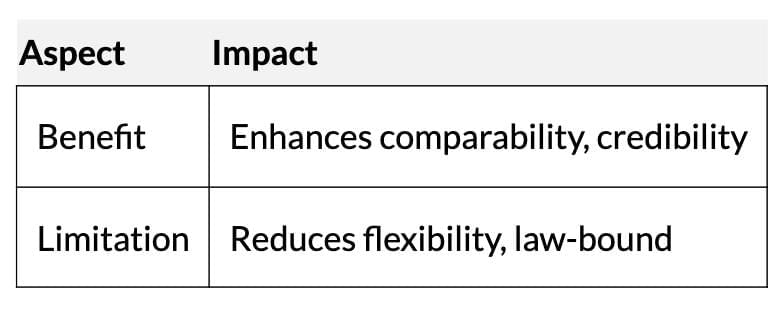

- Guidelines set by ICAI for recognising, measuring, and disclosing transactions.

- Ensure uniformity, comparability, and reliability in financial statements.

- Standardise treatments, enhance credibility.

- Facilitate inter-firm/inter-period comparisons.

- Require beneficial disclosures for stakeholders.

- Reduce flexibility in choosing treatments.

- Must comply with existing laws.

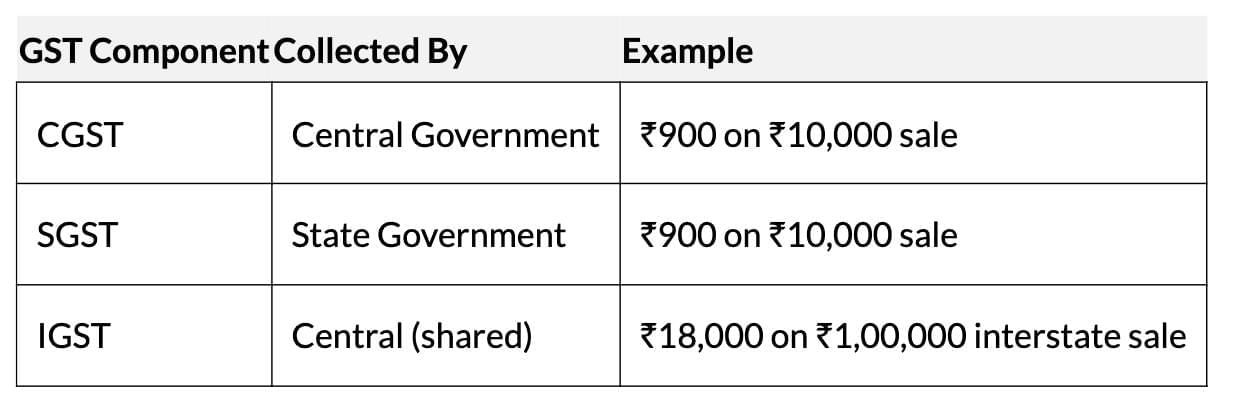

Goods and Services Tax (GST)

- GST is a consumption-based tax on goods/services, applied at each value-added stage with input tax credit.

- CGST: Central government tax, replaces excise/sales tax.

- SGST: State government tax, replaces VAT/entertainment tax.

- IGST: Tax on interstate transactions, shared between central/state governments.

- Example: Punjab dealer sells ₹10,000 goods in Punjab (18% GST): ₹900 CGST, ₹900 SGST; Madhya Pradesh dealer sells ₹1,00,000 goods to Rajasthan: ₹18,000 IGST.

- Uniform law/procedure, destination-based, comprehensive levy.

- Minimal tax rates, no additional levies, and eliminates multiple taxation.

- Abolishes multiple taxes, widens tax base, reduces compliance costs.

- Eliminates cascading effect, boosts manufacturing, enhances exports.

The document Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce is a part of the Commerce Course Accountancy Class 11.

All you need of Commerce at this link: Commerce

|

61 videos|227 docs|39 tests

|

FAQs on Short Notes: Theory Base of Accounting - Accountancy Class 11 - Commerce

| 1. What is the theory base of accounting and why is it important? |  |

Ans. The theory base of accounting refers to the fundamental principles and concepts that underpin the field of accounting. It provides a framework for understanding how financial information is recorded, reported, and analyzed. This theoretical foundation ensures consistency and reliability in financial reporting, enhancing the credibility of financial statements. Understanding this base is crucial for accountants as it guides decision-making and helps maintain transparency in financial practices.

| 2. What are generally accepted accounting principles (GAAP)? | |

Ans. Generally Accepted Accounting Principles (GAAP) are a set of rules and standards used in the preparation of financial statements in many countries, including the United States. GAAP encompasses a broad range of accounting practices, including guidelines on revenue recognition, asset valuation, and expense classification. Adhering to GAAP ensures that financial statements are consistent, comparable, and transparent, thereby facilitating informed decision-making by stakeholders.

| 3. Can you explain the basic accounting concepts? | |

Ans. Basic accounting concepts are fundamental principles that guide the recording and reporting of financial transactions. Some key concepts include the accrual concept (recognizing revenue and expenses when they occur, not when cash is exchanged), the going concern concept (assuming a company will continue to operate indefinitely), and the consistency concept (using the same accounting methods over time). These concepts ensure that financial information is presented in a clear and consistent manner, aiding stakeholders in making informed decisions.

| 4. What are the different systems of accounting? | |

Ans. The two primary systems of accounting are cash basis accounting and accrual basis accounting. In cash basis accounting, revenues and expenses are recorded only when cash is received or paid. Conversely, accrual basis accounting records revenues and expenses when they are earned or incurred, regardless of cash transactions. Most businesses prefer accrual accounting as it provides a more accurate picture of financial performance and position.

| 5. What is the significance of accounting standards and how do they relate to GST? | |

Ans. Accounting standards are authoritative guidelines that govern how financial transactions should be recorded and reported. They ensure consistency and transparency in financial reporting across different entities. The Goods and Services Tax (GST) impacts accounting standards as it requires businesses to account for tax liabilities and input tax credits accurately. Proper adherence to accounting standards ensures compliance with GST regulations, allowing businesses to manage their tax obligations effectively.

About this Document

4.68/5

Rating

Sep 04, 2025

Last updated

Related Exams

Document Description: Short Notes: Theory Base of Accounting for Commerce 2025 is part of Accountancy Class 11 preparation.

The notes and questions for Short Notes: Theory Base of Accounting have been prepared according to the Commerce exam syllabus. Information about Short Notes: Theory Base of Accounting covers topics

like Introduction, Accounting Process and Consistency, Theory Base of Accounting, Generally Accepted Accounting Principles (GAAP), Basic Accounting Concepts, Systems of Accounting, Basis of Accounting, Accounting Standards, Goods and Services Tax (GST) and Short Notes: Theory Base of Accounting Example, for Commerce 2025 Exam. Find important definitions, questions, notes, meanings, examples, exercises and tests below for Short Notes: Theory Base of Accounting.

Introduction of Short Notes: Theory Base of Accounting in English is available as part of our Accountancy Class 11

for Commerce & Short Notes: Theory Base of Accounting in Hindi for Accountancy Class 11 course.

Download more important topics related with notes, lectures and mock test series for Commerce

Exam by signing up for free. Commerce: Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce

Description

Full syllabus notes, lecture & questions for Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce - Commerce | Plus excerises question with solution to help you revise complete syllabus for Accountancy Class 11 | Best notes, free PDF download

Information about Short Notes: Theory Base of Accounting

In this doc you can find the meaning of Short Notes: Theory Base of Accounting defined & explained in the simplest way possible. Besides explaining types of

Short Notes: Theory Base of Accounting theory, EduRev gives you an ample number of questions to practice Short Notes: Theory Base of Accounting tests, examples and also practice Commerce

tests

Related Searches

MCQs

,past year papers

,practice quizzes

,video lectures

,Previous Year Questions with Solutions

,Exam

,Semester Notes

,mock tests for examination

,Sample Paper

,Viva Questions

,study material

,Important questions

,Free

,Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce

,shortcuts and tricks

,Objective type Questions

,Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce

,Extra Questions

,Short Notes: Theory Base of Accounting | Accountancy Class 11 - Commerce

,Summary

,ppt

;

Additional Information about Short Notes: Theory Base of Accounting for Commerce Preparation

Short Notes: Theory Base of Accounting Free PDF Download

The Short Notes: Theory Base of Accounting is an invaluable resource that delves deep into the core of the Commerce exam.

These study notes are curated by experts and cover all the essential topics and concepts, making your preparation more efficient and effective.

With the help of these notes, you can grasp complex subjects quickly, revise important points easily,

and reinforce your understanding of key concepts. The study notes are presented in a concise and easy-to-understand manner,

allowing you to optimize your learning process. Whether you're looking for best-recommended books, sample papers, study material,

or toppers' notes, this PDF has got you covered. Download the Short Notes: Theory Base of Accounting now and kickstart your journey towards success in the Commerce exam.

Importance of Short Notes: Theory Base of Accounting

The importance of Short Notes: Theory Base of Accounting cannot be overstated, especially for Commerce aspirants.

This document holds the key to success in the Commerce exam.

It offers a detailed understanding of the concept, providing invaluable insights into the topic.

By knowing the concepts well in advance, students can plan their preparation effectively.

Utilize this indispensable guide for a well-rounded preparation and achieve your desired results.

Short Notes: Theory Base of Accounting

Short Notes: Theory Base of Accounting Notes offer in-depth insights into the specific topic to help you master it with ease.

This comprehensive document covers all aspects related to Short Notes: Theory Base of Accounting.

It includes detailed information about the exam syllabus, recommended books, and study materials for a well-rounded preparation.

Practice papers and question papers enable you to assess your progress effectively.

Additionally, the paper analysis provides valuable tips for tackling the exam strategically.

Access to Toppers' notes gives you an edge in understanding complex concepts.

Whether you're a beginner or aiming for advanced proficiency, Short Notes: Theory Base of Accounting Notes on EduRev are your ultimate resource for success.

Short Notes: Theory Base of Accounting Commerce Questions

The "Short Notes: Theory Base of Accounting Commerce Questions" guide is a valuable resource for all aspiring students preparing for the

Commerce exam. It focuses on providing a wide range of practice questions to help students gauge

their understanding of the exam topics. These questions cover the entire syllabus, ensuring comprehensive preparation.

The guide includes previous years' question papers for students to familiarize themselves with the exam's format and difficulty level.

Additionally, it offers subject-specific question banks, allowing students to focus on weak areas and improve their performance.

Study Short Notes: Theory Base of Accounting on the App

Students of Commerce can study Short Notes: Theory Base of Accounting alongwith tests & analysis from the EduRev app,

which will help them while preparing for their exam. Apart from the Short Notes: Theory Base of Accounting,

students can also utilize the EduRev App for other study materials such as previous year question papers, syllabus, important questions, etc.

The EduRev App will make your learning easier as you can access it from anywhere you want.

The content of Short Notes: Theory Base of Accounting is prepared as per the latest Commerce syllabus.

|

© EduRev

|

Education Revolution

|

|

Signup to see your scores

go up within 7 days!

Access 1000+ FREE Docs, Videos and Tests

Takes less than 10 seconds to signup