Registration | Goods and Services Tax (GST) - B Com PDF Download

GST Registration Overview

The registration of an assessee or "taxable person" is the first step in any tax law. It is a key requirement for identifying the business for tax purposes and ensuring compliance with regulations.

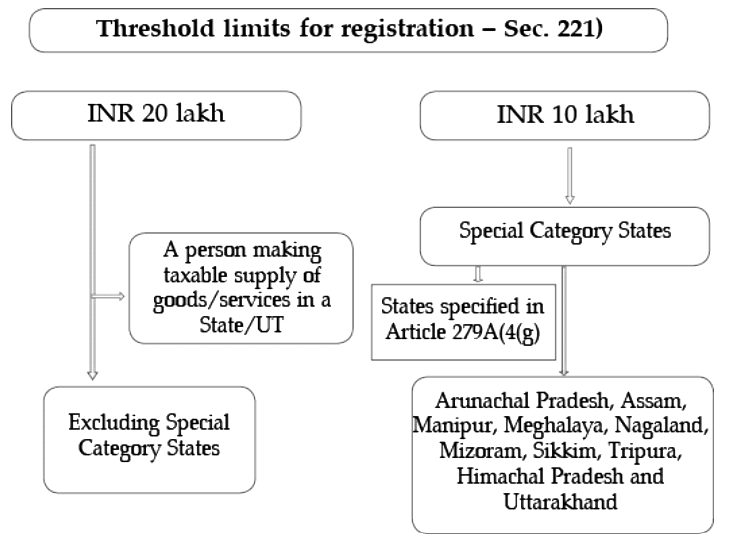

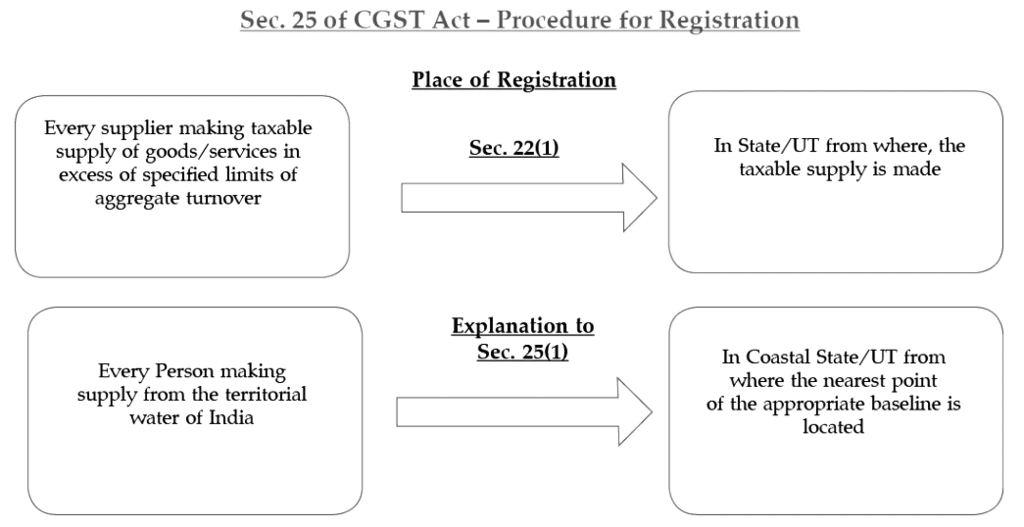

The CGST Act mandates that every supplier making taxable supplies must register. Any supplier whose total turnover exceeds ₹20 lakh in a financial year is required to register. However, for businesses operating in certain states—namely Himachal Pradesh, Uttarakhand, Manipur, Arunachal Pradesh, Assam, Jammu & Kashmir, Meghalaya, Mizoram, Nagaland, Sikkim, and Tripura—the registration threshold is reduced to ₹10 lakh.

When calculating the turnover for registration, the supply of goods by a registered job-worker, after completing job-work, is treated as the supply of goods by the "principal" and should not be included in the job-worker’s aggregate turnover for registration purposes.

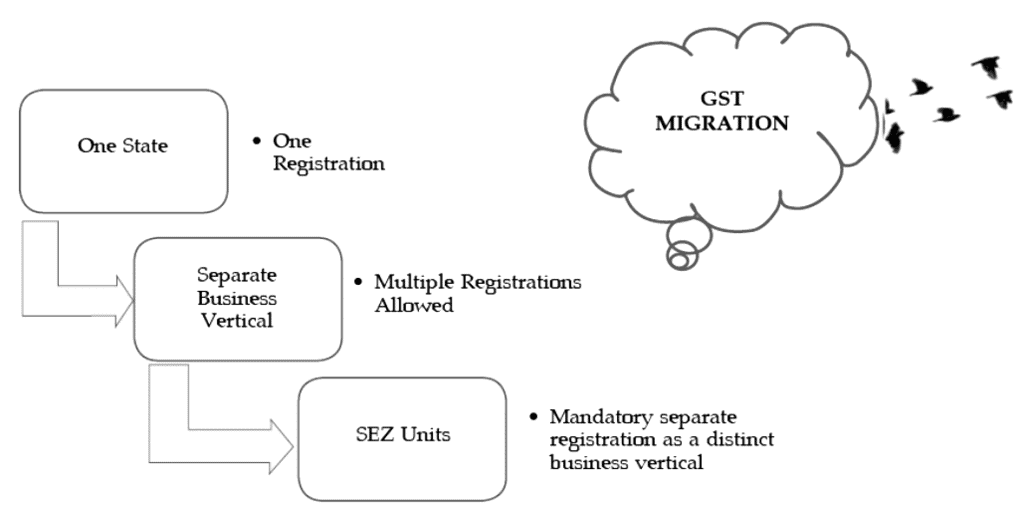

- Under GST, businesses must register in each state where they make taxable sales. If a person sells taxable goods or services in multiple states, they need to register separately in each state once their total earnings exceed the threshold limit, taking into account sales from all states.

- If a person makes taxable sales from different locations within the same state, only one registration is needed for that state. However, if they have different business verticals, they can register multiple times within that state.

- When registering, a taxpayer must choose one location as the principal place of business and list all other locations as additional places of business.

- The registration application must be filed within 30 days from when the requirement to register arises.

- A business vertical is a specific part of a business that provides different goods or services. Each vertical has its own risks and returns compared to others. To identify a business vertical, factors such as the type of goods or services, production methods, customer types, distribution channels, and the regulatory environment (like banking, insurance, or public utilities) are taken into account.

- Businesses that are already registered under Excise, VAT, or Service Tax cannot claim exemptions from the threshold limit. They must switch to GST and obtain provisional registration from GSTN before the set date, even if their earnings are below the threshold limit.

- These businesses can choose not to get provisional registration if their sales do not fall under GST or if they are below the threshold limit.

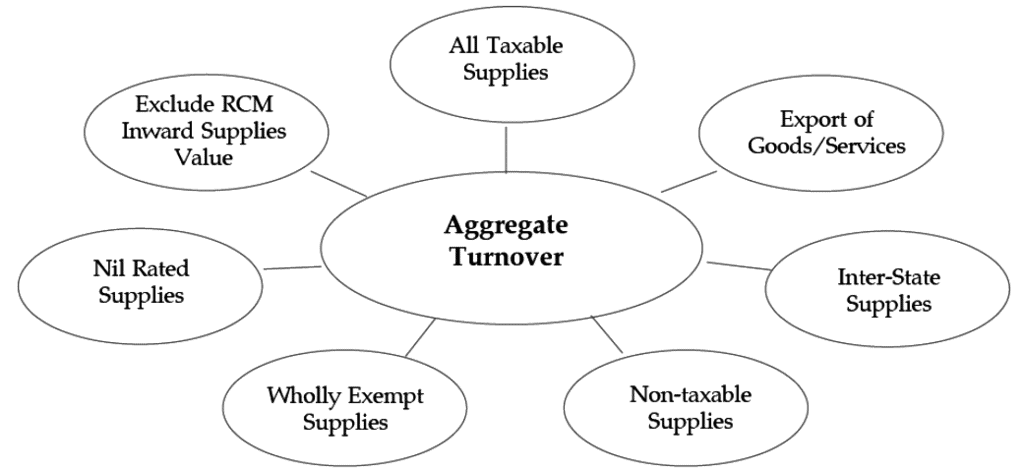

Aggregate turnover refers to the total value of all taxable supplies, exempt supplies, exports of goods or services, and inter-state supplies made by a person with the same Permanent Account Number (PAN), calculated on an all-India basis. However, the following are excluded from this calculation:

- Central Tax (CGST)

- State Tax (SGST)

- Union Territory Tax (UTGST)

- Integrated Tax (IGST)

- Cess

Additionally, the value of inward supplies on which tax is payable under reverse charge is also excluded from the aggregate turnover.

A Special Economic Zone (SEZ) unit or developer must apply for registration separately, treating it as a distinct business vertical from other units located outside the SEZ.

A casual taxable person or a non-resident taxable person must apply for registration at least 5 days before starting their business activities. A casual taxable person refers to someone who occasionally makes taxable supplies of goods or services (or both) in a state or Union Territory where they do not have a fixed place of business. A non-resident taxable person is someone who occasionally conducts taxable transactions involving the supply of goods or services (or both) for business purposes but does not have a fixed place of business or residence in India.

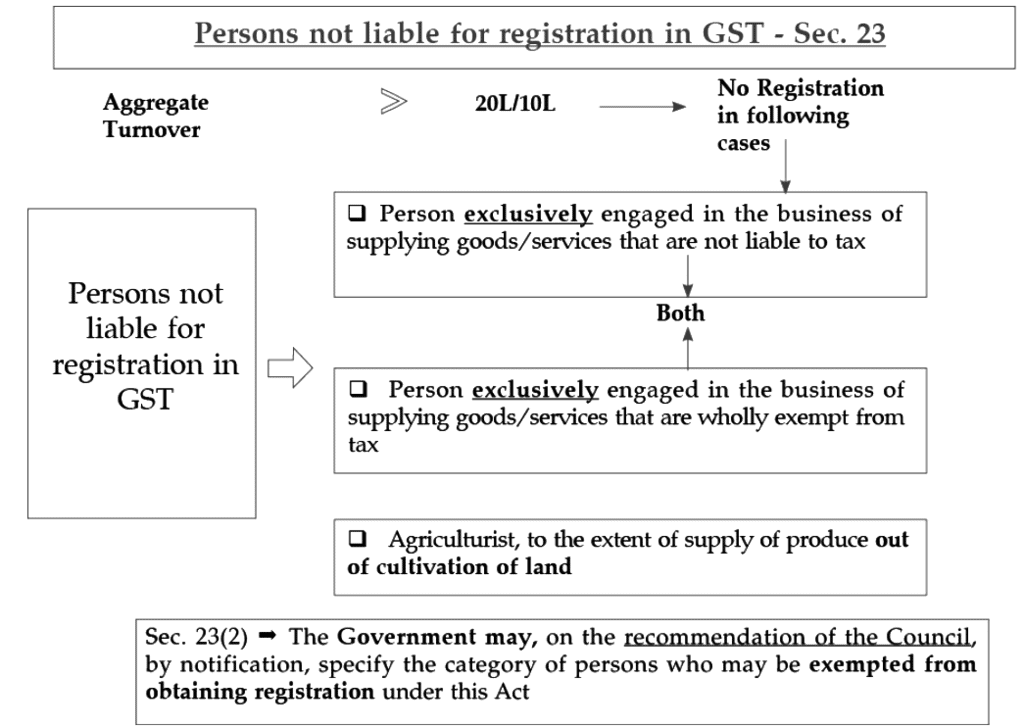

Persons Not Liable for Registration in GST

Categories of Persons Required to be Registered Irrespective of the Threshold

- Person making any inter-State taxable supply: Individuals or businesses involved in taxable supplies between different states are required to register, regardless of the threshold.

- Casual taxable person making taxable supply: Those making taxable supplies on a casual basis, without a fixed place of business, must register.

- Persons required to pay tax under reverse charge: Entities obligated to pay tax under the reverse charge mechanism are mandated to register.

- Electronic commerce operator: Operators facilitating supplies on behalf of other suppliers, particularly for notified services, are liable to register.

- Non-resident taxable person: Non-resident individuals or businesses making taxable supplies in India are required to register.

- Persons required to deduct tax at source under GST: Entities mandated to deduct tax at source under GST provisions must register.

- Persons supplying on behalf of others: Individuals or businesses supplying goods or services on behalf of other registered taxable persons, whether as agents or otherwise, are required to register.

- Input service distributor: Entities acting as input service distributors need to register.

- Every electronic commerce operator: All electronic commerce operators are required to register.

- Persons supplying online information and database access: Individuals or businesses supplying online information and database access services from outside India to persons in India, other than registered taxable persons, must register.

- Other persons as notified: Any other person or class of persons notified by the Central Government or State Government on the recommendations of the Council must register.

Persons Not Liable for Registration

- Exclusive Suppliers of Non-Taxable or Exempt Goods/Services: Individuals engaged solely in providing goods or services that are not subject to tax or are wholly exempt from tax under the CGST Act or the Integrated Goods and Services Tax Act are not liable for registration.

- Agriculturists: Farmers supplying produce from the cultivation of their land are not liable for registration in this context.

- Government Notification: The Government, based on the recommendations of the Council, has the authority to specify categories of persons who may be exempted from obtaining registration under this Act through a notification.

Voluntary Registration

- Option for Voluntary Registration: There are provisions that allow individuals or entities to register voluntarily under this Act, even if they are not required to do so.

Deemed Registration and Cancellation of Registration Certificate

- Deemed Registration: Any grant of registration or Unique Identity Number under SGST or UTGST shall be construed as grant of registration under CGST. Similarly, any grant of registration or Unique Identity Number under CGST shall be construed as grant of registration under SGST or UTGST.

- Rejection of Application: Any rejection of application for registration or cancellation or revocation of registration shall be treated likewise.

Transfer of Business and Registration

- Registration Liability: A transferee or successor of a business on an ongoing concern basis shall be liable to be registered from the date of transfer or succession.

- Transfer Due to Amalgamation or Demerger: In cases of transfer due to a scheme or arrangement for amalgamation or demerger sanctioned by a High Court, the transferee shall be liable to be registered from the date the Registrar of Companies issues a certificate of incorporation reflecting the High Court's order.

- Non-Transferability of Registration Certificate: This indicates that the Registration Certificate issued to an individual is not transferable to another party.

Special Provisions for Casual and Non-Resident Taxable Persons

Registration Validity: The Certificate of Registration for casual and non-resident taxable persons is valid for 90 days from the registration date or a shorter period specified in the application. Extension: An extension of up to 90 days may be granted under sufficient circumstances. Tax Deposit: An advance tax deposit, reflecting the estimated tax liability for the registration period, will be credited to the electronic cash ledger.

Suo Motu Registration by the Department

If during a survey, inspection, search, enquiry, or any other proceeding under the Act, it is discovered that a person obligated to register has failed to do so, the proper officer may register the individual on a temporary basis and issue an order in FORM GST REG-12.

- Effective Date: The registration will be effective from the date of the order.

- Application Requirement: The registered individual is required to apply for formal registration within 30 days from the date of the temporary order, unless an appeal against the order is filed.

Amendment to Registration

There are several situations where the registration issued by the competent authority needs to be amended to reflect real-time changes. In such cases, every registered taxable person must inform any changes in the information provided at the time of registration within 15 days of such changes.

The proper officer cannot reject the request for amendment without giving a reasonable opportunity to be heard, following the principles of natural justice.

Cancellation of Registration

A granted registration can be cancelled by the proper officer either on their own initiative or at the request of the registered person under the following circumstances:

- If the business is discontinued, fully transferred for any reason (including the death of the proprietor), amalgamated with another legal entity, demerged, or otherwise disposed of.

- If there is any change in the constitution of the business.

- If the taxable person is no longer liable to be registered.

Registration may be cancelled retrospectively if the proper officer deems it appropriate in certain situations, such as:

- If the registered person has violated provisions of the Act or Rules.

- If a person paying tax under the Composition Scheme has not filed returns for three consecutive tax periods.

- If any taxable person has not filed returns for a continuous period of six months.

- If a person who has voluntarily registered has not commenced business within six months from the date of registration.

- If registration has been obtained through fraud, willful misstatement, or suppression of facts.

The cancellation of registration does not affect the taxable person's liability to pay tax and other dues under the Act for any period prior to the date of cancellation, regardless of whether such tax and dues are determined before or after the date of cancellation.

Upon cancellation of registration, the registered taxable person must pay an amount equivalent to the input tax credit for inputs held in stock and inputs contained in semi-finished or finished goods held in stock on the day immediately preceding the date of cancellation, or the output tax payable on such goods, whichever is higher. This payment can be made by debiting the electronic credit or electronic cash ledger.

In the case of capital goods, the taxable person must pay an amount equal to the input tax credit taken on the capital goods, reduced by a prescribed percentage, or the tax on the transaction value of such capital goods, whichever is higher.

Revocation of Cancellation of Registration

- Registered taxable persons whose registration has been cancelled can apply to the proper officer for revocation of the cancellation within thirty days from the date of service of the cancellation order.

- The proper officer must provide a show cause notice and give the person a reasonable opportunity to be heard before rejecting the application for revocation.

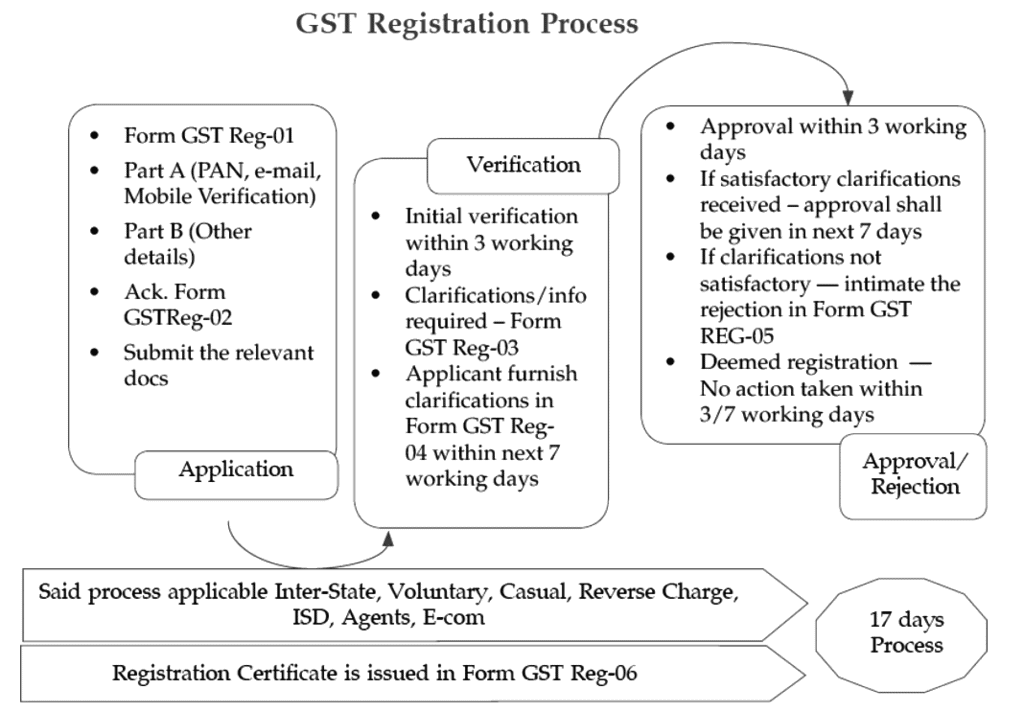

Procedure for Registration

Online Application:

- Registered taxable persons need to submit an online application in FORM GST REG-01.

- Provide details such as PAN, mobile number, email address, State or UT, and other required documents.

- Ensure the application is electronically verified and signed.

Special Cases:

- Persons liable to deduct TDS or collect TCS should apply using FORM GST REG-07.

- Non-resident taxable persons must apply in FORM GST REG-09.

Acknowledgment:

- Upon successful submission, an acknowledgment will be generated in FORM GST REG-02.

Processing:

- The proper officer will either grant registration or issue a notice in FORM GST REG-03 for additional information within 3 working days.

- If a notice is issued, the applicant must respond in FORM GST REG-04 within 7 working days.

Granting Registration:

- If the applicant fails to respond, the proper officer may reject the application in FORM GST REG-05.

- If satisfied with the provided information, registration may be granted within 7 working days.

Issuance of Registration Certificate:

- The Registration Certificate will be issued in FORM GST REG-06.

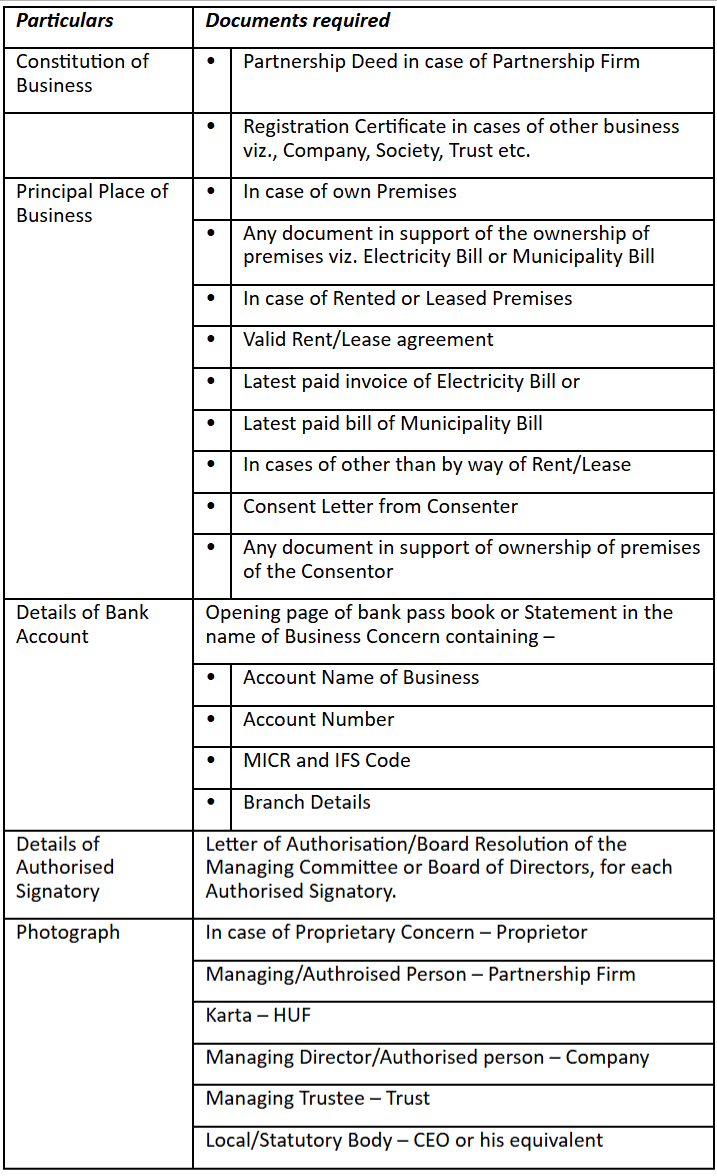

Documents Required For Registration

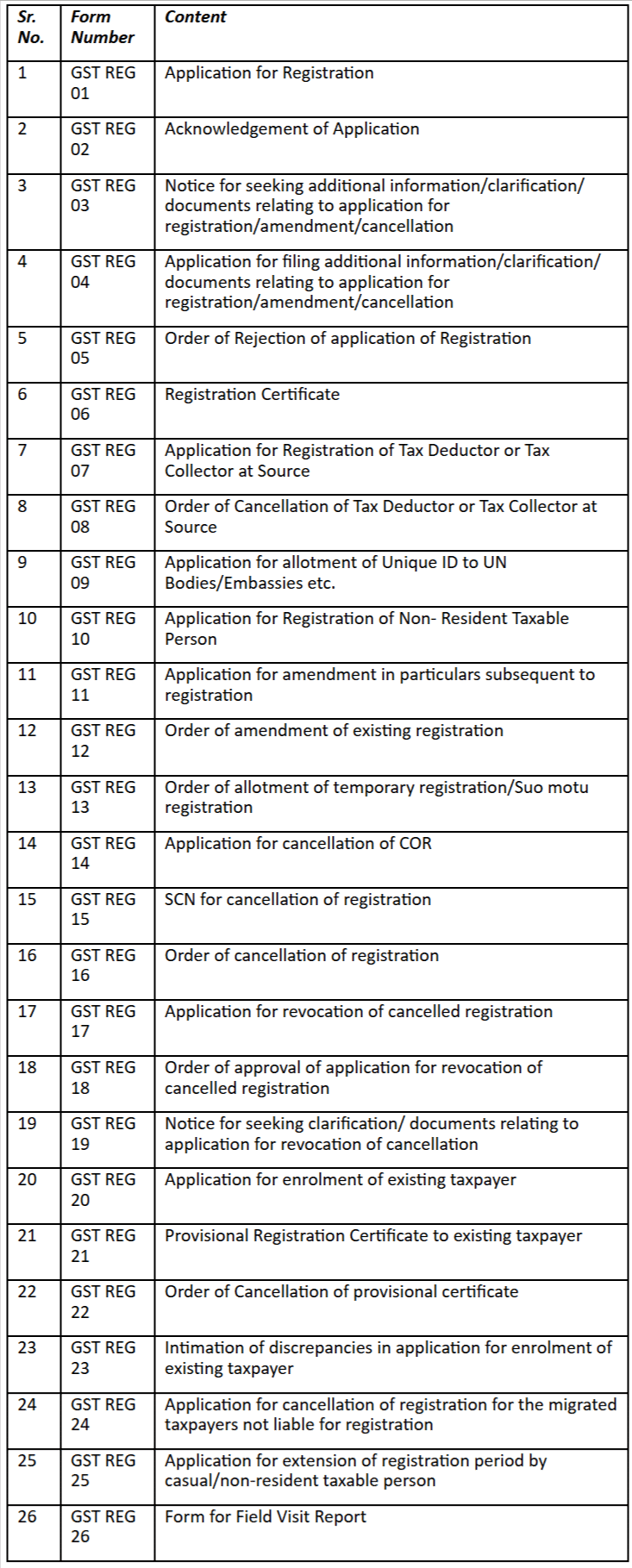

List of Forms for Registration

|

19 videos|83 docs|14 tests

|

FAQs on Registration - Goods and Services Tax (GST) - B Com

| 1. Why is registration necessary under GST? |  |

| 2. What is the Goods and Services Tax Identification Number (GSTIN)? | |

| 3. Who is not liable for registration under GST according to Section 23? | |

| 4. What are the circumstances that require compulsory registration under Section 24? | |

| 5. How does the nature of registration impact a business's operations? | |

MCQs

,Registration | Goods and Services Tax (GST) - B Com

,study material

,Exam

,practice quizzes

,Viva Questions

,Extra Questions

,Registration | Goods and Services Tax (GST) - B Com

,past year papers

,Summary

,ppt

,mock tests for examination

,video lectures

,Free

,shortcuts and tricks

,Sample Paper

,Semester Notes

,Objective type Questions

,Registration | Goods and Services Tax (GST) - B Com

,Important questions

,Previous Year Questions with Solutions

;

Registration Free PDF Download

Importance of Registration

Registration Notes

Registration B Com Questions

Study Registration on the App

|

© EduRev

|

Education Revolution

|

|