Introduction, Genesis & Shortcomings of GST | Goods and Services Tax (GST) - B Com PDF Download

| Table of contents |

|

| Introduction |

|

| Introduction of GST in India |

|

| Constitutional Amendment for GST |

|

| Legislative Framework for GST in India |

|

| Structure of GST |

|

| Disadvantages of GST |

|

Introduction

The Goods and Services Tax (GST) is considered one of the most significant tax reforms in India since independence. It is a groundbreaking indirect tax reform aimed at creating a unified national market by eliminating inter-state trade barriers. GST has absorbed and included multiple indirect taxes previously imposed by both the central and state governments.

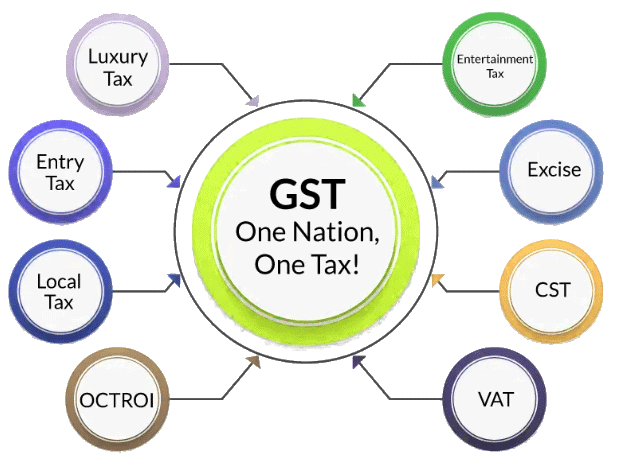

Taxes Subsume by GST

Central Taxes:

- Central Excise Duty

- Additional Excise Duty

- Service Tax

- Surcharge and Cess

- Central Sales Tax

State Taxes:

- State VAT

- Entertainment Tax

- Entry Tax

- Luxury Tax

- Purchase Tax

Historical Background:

- GST was first introduced in France in 1954.

- Over the next 62 years, around 160 countries adopted GST in various forms.

- While GST is commonly known for a single model, countries like Canada and Brazil have implemented a dual model.

India’s Implementation:

- India has adopted a dual GST system, where the tax is imposed concurrently by both the central and state governments.

Introduction of GST in India

- 2004: The idea of Goods and Services Tax (GST) in India was proposed by the Kelkar Task Force.

- 2007: Union Finance Minister P. Chidambaram announced the introduction of GST in India during the central Budget presentation.

- 2014: The NDA government introduced the Constitution (122nd Amendment) Bill to facilitate the GST.

- 2016: The Bill received presidential assent on September 8, 2016, becoming the Constitution (101st Amendment) Act, 2016, which set the stage for GST implementation.

- 2017 (March): Four key GST bills were introduced and passed in the Lok Sabha: Central Goods and Services Tax Bill, Integrated Goods and Services Tax Bill, Union Territory Goods and Services Tax Bill, and Goods and Services Tax (Compensation to States) Bill. These bills received presidential assent on April 12, 2017.

- 2017 (July): GST was implemented across India from July 1, 2017.

Constitutional Amendment for GST

The Constitution (101st Amendment) Act, 2016, enacted on September 8, 2016, brought about significant changes to the Indian Constitution regarding the Goods and Services Tax (GST). Here are the key amendments:

(a) Concurrent Power to Tax: Both Parliament and State legislatures were given concurrent power to make laws for imposing taxes on goods and services.

(b) Scope of GST: GST would be levied on all supplies of goods and services, except for alcoholic liquor for human consumption.

(c) Inter-State Supply: Parliament was granted exclusive power to make laws regarding the goods and services tax on inter-state supply (supply from one state to another).

(d) Place of Supply: Parliament was given the authority to decide the principles for determining the place of supply and when supply takes place in the course of inter-State trade and commerce.

(e) Import Supply: The amendment clarified that the import of goods and services would be deemed as a supply taking place in the course of inter-State trade and commerce.

(f) Central Excise Duty and Sales Tax: Central Excise duty would be imposed on the production of certain items, while respective States would impose Sales tax on their sales. The items include:

- Petroleum crude

- High-speed diesel

- Motor spirit (petrol)

- Natural gas

- Aviation turbine fuel

- Tobacco and tobacco products

(g) GST Council: Article 279A empowered the President of India to constitute the Goods and Services Tax Council (GST Council) under the chairmanship of the Union Finance Minister. The Council is responsible for making recommendations on:

- GST rates

- Valuation and fundamental rules

- Exemptions

- Future changes

- Returns

- Registrations

Legislative Framework for GST in India

In India, there are a total of 35 GST Acts that govern the Goods and Services Tax. These acts are designed to regulate different aspects of GST at the central and state levels.

1. Central Goods and Services Tax (CGST) Act, 2017

- This act is responsible for imposing CGST on the intra-State supply of goods and services.

2. State Goods and Services Tax (SGST) Act, 2017

- Each state in India uses this act to impose SGST on the intra-State supply of goods and services.

3. Union Territory Goods and Services Tax (UTGST) Act, 2017

- This act is applicable in five Union Territories without their own State Legislatures:

- Andaman and Nicobar Islands

- Lakshadweep

- Dadra and Nagar Haveli

- Daman and Diu

- Chandigarh

- The UTGST is levied on the intra-Territory supply of goods and services in these areas.

4. Integrated Goods and Services Tax (IGST) Act, 2017

- This act governs the levy of IGST on inter-State supply of goods and services.

5. Goods and Services Tax (Compensation to States) Act, 2017

- This act provides for the levy of GST Compensation Cess, which is used to compensate states for the loss of revenue due to the implementation of GST.

Structure of GST

- Nature of GST: GST is a single tax levied on the supply of goods and services across India, from the manufacturer to the consumer. It allows for the set-off of taxes paid at previous stages against the output tax.

- Destination-Based Tax: GST is a destination-based consumption tax, meaning the tax benefit (STCG/ UTGST) accrues to the consuming state.

- Dual Tax System: Both the Centre and states impose tax on goods and services simultaneously. The Centre can now tax the sale of goods within a state, while states can tax services.

- Types of Supplies: (1) Intra-State Supply: CGST is payable to the Central Government, and SGST/ UTGST is payable to the State Government or Union Territory where the goods/services are consumed.

(2) Inter-State Supply: IGST is payable to the Central Government. - Administration of GST: The Centre will levy and administer CGST and IGST, while the respective States/ Union Territories will levy and administer SGST. UTGST.

- Treatment of Imports and Exports: Imports are treated as inter-State supply, and IGST is chargeable along with basic Customs duty. Exports, on the other hand, are treated as zero-rated supplies, and no IGST is payable.

- GST Rates and Cess: GST rates are 0.5%, 3%, 5%, 12%, 18%, and 28%. Additionally, a compensation cess is applicable on items like pan masala, coal, aerated water, and motor cars. There is no Education cess, Swachh Bharat cess, or Krishi Kalyan Cess on GST.

- Valuation for GST: GST is calculated on the transaction value of the supply of goods and services, which is the value agreed upon by the parties, subject to certain exceptions.

- Registration under GST: Every supplier making taxable supplies is required to register under GST law.

- Input Tax Credit (ITC): Registered person is entitled to take credit of input tax paid from the output tax, subject to certain restrictions:

Utilisation of IGST: First for IGST, then CGST and SGST/UTGST.

Utilisation of CGST: First for CGST, then IGST.

Utilisation of SGST/UTGST: First for SGST/UTGST, then IGST. - Seamless Credit Flow: Under the GST regime, there is a seamless credit flow for inter-state supplies. This was not possible before GST, where no credit was available for CST paid by the buyer.

The seamless credit flow under GST includes:

Inter-State Supplier: Can set off available credit in IGST, CGST, and SGST/UTGST against IGST payable on inter-state supply.

Buyer in Importing State: Can avail credit of IGST paid on purchase from output tax payable.

Exporting State: Transfers credit of SGST/UTGST utilised for payment of IGST to the Centre.

Centre: Transfers credit of IGST used in payment of SGST/UTGST to the importing state. - Common GST Electronic Portal: Strong IT infrastructure is necessary for the smooth functioning of GST, and the Government has established a common GST Electronic Portal managed by the Goods and Services Network (GSTN). GSTN provides services such as facilitating registration, forwarding returns to authorities, computation and settlement of IGST, matching tax payment details, and providing analysis of taxpayers’ profiles.

Benefits of GST

GST is advantageous for the entire country, benefiting all stakeholders including industries, the government, and consumers. It is expected to lower the costs of goods and services, making them globally competitive. The following are the significant benefits of GST:

- Creation of a Unified National Market: GST aims to transform India into a unified market with common tax rates and compliance procedures, eliminating economic barriers and fostering an integrated national economy.

- Mitigation of Cascading Effects: By consolidating most Central and State indirect taxes into a single tax, GST allows for the credit of taxes paid throughout the entire value chain process. This eradication of "tax on tax" benefits industries significantly.

- Boost to the 'Make in India' Initiative: GST is expected to significantly enhance the 'Make in India' initiative by making domestically produced goods and services more competitive in both national and international markets.

- Increase in Government Revenue: GST is anticipated to increase government revenue by broadening the tax base and improving taxpayer compliance.

Disadvantages of GST

Increased Costs from Software Purchases:

- Businesses must regularly track and update their accounting or ERP software to comply with GST legal and portal updates.

- This can involve significant costs and time commitments for training employees to use new GST software effectively.

- Alternatively, businesses can invest in a GST compliance solution, which also requires financial investment and training.

Risk of Penalties for Non-Compliance:

- Small businesses are still adapting to GST requirements, including issuing GST-compliant invoices, maintaining digital records, and filing returns on time.

- Non-compliance can lead to penalties, making it crucial for businesses to stay updated and compliant with GST regulations.

Increased Operational Costs:

- GST changed the tax payment and return filing process, leading to higher costs for businesses.

- Businesses had to hire tax professionals with GST expertise and train employees in GST compliance, increasing overhead expenses.

- Solutions like ClearGST can help businesses ensure compliance at a lower cost.

Mid-Year Implementation of GST:

- GST was implemented on July 1, 2017, causing businesses to follow the old tax structure for the first three months of the financial year and switch to GST for the remaining period.

- This transition period created confusion and compliance issues for many businesses.

Transition to Online Taxation System:

- Businesses had to move from traditional pen-and-paper invoicing and filing to online return filing and payments, which was challenging for some smaller businesses.

Increased Tax Burden on SMEs:

- Smaller businesses, particularly in manufacturing, face a higher tax burden under GST.

- Previously, only businesses with a turnover exceeding Rs.1.5 crore had to pay excise duty. Now, any business with a turnover exceeding Rs.20 lakh must pay GST.

- SMEs with a turnover up to Rs.75 lakh can opt for the composition scheme, paying only 1% tax on turnover in lieu of GST, but they cannot claim input tax credit.

- This decision between higher taxes or the composition scheme poses a challenge for many SMEs.

|

20 videos|77 docs|14 tests

|

FAQs on Introduction, Genesis & Shortcomings of GST - Goods and Services Tax (GST) - B Com

| 1. What is the purpose of introducing GST in India? |  |

| 2. What constitutional amendment was required to implement GST in India? | |

| 3. What is the legislative framework governing GST in India? | |

| 4. What are the main components of the GST structure? | |

| 5. What are some disadvantages or shortcomings of GST in India? | |

Introduction

,Sample Paper

,Free

,Extra Questions

,past year papers

,ppt

,Introduction

,Viva Questions

,Exam

,Summary

,shortcuts and tricks

,video lectures

,mock tests for examination

,Introduction

,study material

,Important questions

,Genesis & Shortcomings of GST | Goods and Services Tax (GST) - B Com

,MCQs

,practice quizzes

,Genesis & Shortcomings of GST | Goods and Services Tax (GST) - B Com

,Semester Notes

,Previous Year Questions with Solutions

,Genesis & Shortcomings of GST | Goods and Services Tax (GST) - B Com

,Objective type Questions

;

Introduction, Genesis & Shortcomings of GST Free PDF Download

Importance of Introduction, Genesis & Shortcomings of GST

Introduction, Genesis & Shortcomings of GST Notes

Introduction, Genesis & Shortcomings of GST B Com Questions

Study Introduction, Genesis & Shortcomings of GST on the App

|

© EduRev

|

Education Revolution

|

|