Types of Taxes | Goods and Services Tax (GST) - B Com PDF Download

Introduction

Taxation plays a crucial role as a social and economic instrument. To build a strong and sustainable tax system, effective tax administration is essential. The primary goal of taxation is to enhance revenue collection to fund government expenditures, which in turn enables the provision of public goods and services to the population.

- A robust tax administration is necessary to create a strong and sustainable tax collection system. The practice of tax collection dates back to ancient civilizations in Egypt, China, and Mesopotamia. Historical records, such as cuneiform tablets from the ancient Middle East, indicate the fear and respect associated with tax collectors.

- In ancient times, taxes were often collected by powerful individuals from religious or royal backgrounds. Kautilya’s Arthashastra, along with later texts like the Jatakas from the post-Mauryan period, provides detailed insights into taxation and financial administration in India. Kautilya’s work is considered a foundational guide for financial governance. Over time, India’s accounting systems and practices have evolved significantly.

This unit aims to familiarize learners with key aspects of tax administration, different types of taxes, the role of the Goods and Services Tax Council, and the functions of the Central Board of Direct Taxes and the Central Board of Indirect Taxes and Customs.

Tax Administration in India

Tax administration is crucial for ensuring proper tax collection by the government. It involves various functions aimed at managing and overseeing the tax system effectively.

The key functions of tax administration include:

- Taxpayer service: Providing quality taxpayer service is essential for effective enforcement and compliance.

- Taxpayer identification and registration: Issuing Permanent Account Numbers (PAN) to taxpayers for identification purposes.

- Collection of information: Gathering taxpayer information through various means, including taxpayer declarations, information returns, and assessments conducted by the Income Tax Department.

- Search and seizure: Conducting searches and seizures to uncover concealed income and prevent tax evasion by collecting evidence and ascertaining facts.

- Survey operations: The Income Tax Authority has the power to inspect and check books of accounts, stocks, and other relevant documents at the premises of business enterprises.

- Verification of tax returns: Routine verification of tax returns and sending tax refund intimations to taxpayers.

- Computerisation of tax administration: Implementing electronic filing, data interchange, and computerized taxpayer assistance to enhance efficiency and benefit taxpayers.

Collection of Taxes and Accounting

Refund (Vijay Kelkar Committee, 2002)

- The Income Tax Department (ITD) in India was set up according to the Income Tax Act of 1922. Over time, it expanded its structure by establishing the Central Board of Revenue Act to manage the functions outlined in the IT Act. The ITD continued to grow, adapting to the need for specialized functions such as handling appeals and conducting inspections within the Department.

- To reach its current level of efficiency, the ITD underwent various tax reforms over the years. Some of the significant policy, administrative, and technological reforms implemented in recent years include:

(a) Policy Reforms

- Withdrawal or reduction of major tax incentives.

- Introduction of measures for presumptive taxation.

- Simplification of tax laws, especially concerning capital gains.

- Widening the tax base.

(b) Administrative Reforms

- Computerization involving the allocation of a unique identification number to taxpayers, evolving into a unique business identification number.

- Creation of the Tax Information Network (TIN) by the National Securities Depository Limited (NSDL) to modernize the income tax department through information technology for the collection, processing, monitoring, and accounting of direct taxes.

- Introduction of e-TDS (Tax Deducted at Source) and e-TCS (Tax Collected at Source) facilities.

- Realignment of human resources to meet the changing business needs of the organization.

(c) Technological Reforms

Computerization in the Income Tax Department began in 1981 with the establishment of the Directorate of Income Tax (Systems). Initially, it focused on the processing of challans, and computer centers were set up in metropolitan cities, later expanded to 33 major cities. The scope of computerization was broadened to include the allotment of Permanent Account Numbers (PAN), Tax Deduction Account Numbers (TAN), and payroll accounting.

(d) Restructuring of the ITD

- In 2000, the ITD was restructured to enhance effectiveness and productivity, increase revenue collection, improve services to taxpayers, reduce expenditure by downsizing the workforce, introduce information technology, and standardize work norms.

Recent Developments

- In September 2021, the Government of India launched a new e-filing web portal for taxpayers to streamline the filing process.

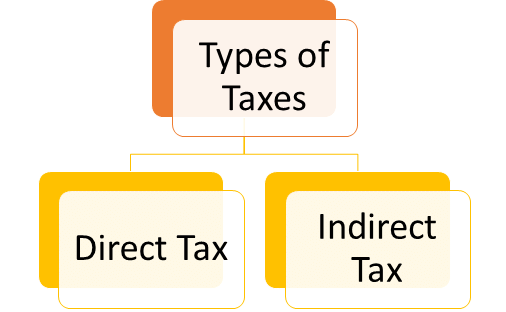

Types of Taxes in India

Taxes play a crucial role as a primary source of revenue for the government, facilitating the financing of various goods and services. In India, taxes are categorized into two main types: direct taxes and indirect taxes. Direct taxes are imposed by the central government, while indirect taxes are levied by the states. Let us take a brief look at the various taxes that come under these two categories.

1. Direct Taxes

The Government of India imposes several types of direct taxes, including:

- Corporation Tax: This tax is levied on domestic and foreign organizations operating in India.

- Personal Income Tax: This tax is based on the personal income of individuals and varies according to factors such as age, income level, and physical disability. The tax slabs can change over time, requiring individuals to file their income tax returns annually.

- Capital Gains Tax: This tax is imposed on the sale of assets or investments, such as houses, bonds, and shares. The tax is determined by the holding period of the asset and is classified into short-term and long-term capital gains.

- Estate Tax: Also known as inheritance tax, this tax is applied to the value of an estate or money left behind by a deceased individual.

2. Indirect Taxes

- Since 2017, the primary indirect tax in India is the Goods and Services Tax (GST), which has replaced various other indirect taxes that existed prior to the 101st Constitutional Amendment Act, 2016. The introduction of GST is considered a significant tax reform in India.

- GST came into effect on July 1, 2017, after a lengthy period of discussions and debates spanning nearly a decade. It is based on the principle of “one nation, one tax, one market.” GST is a multi-stage, destination-based tax imposed on every value addition, and India is now part of a global cluster of 140 countries implementing GST.

- The GST system in India is founded on cooperative federalism and economic integration, aiming to reduce corruption and enhance transparency. It applies to domestic consumption and has transformed India into a unified market, benefiting industries, the government, and consumers alike. Additionally, GST is a technology-driven tax that minimizes human intervention to curb corruption. Being a dual model tax, GST is applicable in all states and Union territories of India.

Goods and Services Tax Council

Goods and Services Tax (GST) is an indirect tax levied on the supply of goods and services. It is a multi-stage, destination-oriented tax that has replaced various indirect taxes such as VAT, excise duty, service tax, and luxury tax at the central, state, and union territory levels.

There are four types of GST:

- State GST (SGST)

- Central GST (CGST)

- Integrated GST (IGST)

- Union Territory GST (UGST)

The Goods and Services Tax Council (GST Council) is a constitutional body responsible for making recommendations to the union and state governments regarding GST. It was established to modify, regulate, and reconcile GST in India. The council is tasked with various responsibilities, including:

- Inclusion of taxes, cesses, and surcharges in GST

- Exemption of certain goods and services

- Determining GST rates

- GST laws and principles of levy

- Apportionment of GST

- Implementation and regulation of GST

The GST Council is chaired by the Union Finance Minister, with other members including the Union Minister of State for Revenue or Finance and the Finance or Taxation Ministers of the States. The council was to be constituted by the President within 60 days of the commencement of Article 279A of the amended Constitution. According to Article 279A, the GST Council consists of:

- Union Finance Minister (Chairperson)

- Union Minister of State in charge of Revenue or Finance

- Minister in charge of Finance or Taxation or any other Minister nominated by each State Government

The Cabinet also decided to appoint the Secretary (Revenue) as the Ex-Officio Secretary to the GST Council and the Chairperson of the Central Board of Excise and Customs (CBEC) as a permanent invitee (non-voting) to all GST Council proceedings. Additionally, the Cabinet allocated funds for the recurring and non-recurring expenses of the GST Council Secretariat, which will be entirely borne by the central government. The Secretariat will be managed by officers on deputation from both the Central and State Governments.

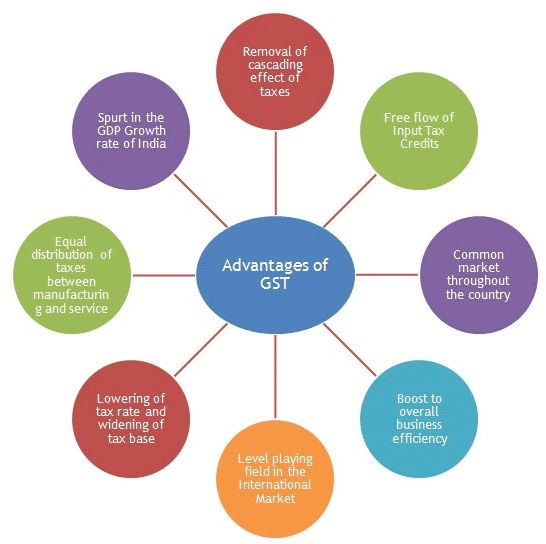

Goods and Services Tax : Advantages

GST, the indirect tax in India, offers numerous advantages across various sectors.

1. Advantages for the Government:

- Unified Market and Cascading Effect: GST aims to create a unified national market, attracting foreign investment and supporting the "Make in India" initiative. It also reduces the cascading effect of taxes by allowing Input Tax Credit (ITC) across goods and services at every stage of supply.

- Harmonisation and Compliance: GST harmonises laws, procedures, and tax rates between the centre and states, as well as among states. It enhances compliance by requiring online filing of all returns and verification of input credits, facilitating better monitoring of transactions throughout the supply chain.

- Uniformity and Common Procedures: The standardisation of SGST and IGST rates helps reduce tax evasion by eliminating rate arbitrage between neighbouring states and intra/inter-state sales. GST also establishes common procedures for taxpayer registration, tax refunds, and tax returns, providing greater certainty in the taxation system.

- Human Interface: Increased use of information technology in GST reduces human interaction between taxpayers and tax authorities, thereby minimising corruption.

- Economic Growth and Poverty Reduction: GST is expected to boost exports, manufacturing, and employment, leading to increased GDP and economic growth. This, in turn, contributes to poverty alleviation by creating more jobs and financial resources.

2. Advantages to Trade and Industry:

- Simplicity and Ease: GST simplifies the tax regime with fewer exemptions, making it easier to do business. It reduces the multiplicity of taxes, leading to greater uniformity and simplicity.

- Elimination of Double Taxation: GST eliminates double taxation in sectors like works contracts, software, and hospitality, and mitigates the cascading effect of taxes by allowing ITC across goods and services at all stages of supply.

- Reduction in Compliance Costs: GST reduces compliance costs by eliminating the need for multiple record-keeping for various taxes, saving resources and manpower.

- Efficiency in Exports: GST enhances the neutralisation of taxes for exports, making Indian products more competitive in the global market and boosting exports.

- Simplified Procedures: GST offers simplified and automated procedures for registration, returns, refunds, tax payments, and other processes.

- Reduction in Tax Burden: GST is expected to lower the average tax burden on goods and services, leading to increased consumption and production, which benefits the manufacturing sector.

3. Advantages to Consumers:

- Transparency: GST promotes transparency in pricing due to the seamless flow of input tax credit between manufacturers, retailers, and service providers.

- Price Reduction: Over the long term, GST is likely to reduce the prices of goods and commodities by minimising the cascading impact of taxation.

- Exemptions:. significant segment of small retailers may be exempt from tax or subjected to low tax rates under a compounding scheme, resulting in lower prices for consumers.

- Reduction in Poverty: GST contributes to poverty reduction by generating more employment opportunities and increasing financial resources.

4. Advantages to States:

- Tax Base and Power to Tax: GST expands the tax base for states, allowing them to tax the entire supply chain from manufacturing to retail. States gain the power to tax services, previously under the central government's purview, boosting revenue and accessing the rapidly growing service sector.

- Favouring Consuming States: As a destination-based consumption tax, GST benefits consuming states.

- Development of States: GST improves the overall investment climate in the country, benefiting the development of states.

- Better Compliance: Uniformity in SGST and IGST rates reduces incentives for tax evasion by eliminating rate arbitrage between neighbouring states and intra/inter-state sales. Improved compliance levels among taxpayers contribute to better revenue collection for states.

Role of Central Board of Direct Taxes and Central Board of Indirect Taxes and Customs

The Ministry of Finance in India is responsible for levying and collecting direct and indirect taxes, with the assistance of the Central Board of Direct Taxes (CBDT) and the Central Board of Indirect Taxes and Customs (CBIC).

The Central Board of Direct Taxes

- Overview: The Central Board of Direct Taxes (CBDT) operates under the Central Board of Revenue Act, 1963. It plays a crucial role in formulating policies and administering direct taxes in India.

- Historical Background: The Central Board of Revenue was established by the Central Board of Revenue Act, 1924, to oversee tax administration. Initially responsible for both direct and indirect taxes, the Board was divided into the CBDT and the Central Board of Excise and Customs in 1964 due to the growing complexity of tax administration.

Composition: The CBDT consists of a Chairman and six members, each responsible for specific areas:

- Chairman

- Member (Income-tax)

- Member (Legislation & Computerisation)

- Member (Personnel & Vigilance)

- Member (Investigation)

- Member (Revenue)

- Member (Audit & Judicial)

Functions: The CBDT provides inputs for the policy, planning, and administration of direct taxes through the Income Tax Department. It is responsible for the levy and collection of direct taxes in India.

Role and Functions of CBDT

The Central Board of Direct Taxes (CBDT) is responsible for formulating policies related to the statutory functions of the Board and the Union Government under various direct tax laws.

The functions and role of CBDT include:

- Organisation: Determining the structure and setup of the Income-tax Department.

- Methods and Procedures: Establishing procedures for the Board's work.

- Tax Management: Implementing measures for assessments, tax collection, and preventing tax evasion and avoidance.

- Personnel Management: Overseeing recruitment, training, and service conditions of Income-tax Department personnel.

- Targets and Priorities: Setting targets and priorities for assessments and tax collection.

- Rewards Policy: Developing policies for grants of rewards and appreciation certificates.

- Miscellaneous: Addressing any other matters referred by the Chairman or Board members.

Central Board of Indirect Taxes and Customs (CBITC)

- The Central Board of Indirect Taxes and Customs (CBIC), formerly known as the Central Board of Excise and Customs (CBEC), is a key part of the Department of Revenue under the Ministry of Finance, Government of India. The CBEC was renamed to CBIC in 2018 following the implementation of the Goods and Services Tax (GST).

- The CBIC is responsible for formulating policies related to the levy and collection of Customs duties, Central Excise duties, Central Goods and Services Tax (CGST), Integrated Goods and Services Tax (IGST), and prevention of smuggling. It also handles the administration of these taxes and matters related to narcotics control.

- The Board oversees various subordinate organizations, including Custom Houses, Central Excise and Central GST Commissionerates, and the Central Revenues Control Laboratory.

Structure of CBIC

The CBIC is headed by the following officials:

- Chairperson

- Member (Customs)

- Member (Legal, CX, and ST)

- Member (GST and Tax Policy)

- Member (Administration and Vigilance)

- Member (Investigation)

- Member (IT and Taxpayer Services)

Vision and Mission

- Vision: The CBIC aims to foster India’s socio-economic growth by formulating and implementing progressive indirect tax policies with a stakeholder-centric approach while safeguarding the country's borders.

- Mission: The CBIC is dedicated to establishing a robust indirect tax and border control administration that delivers services in a simple, predictable, fair, transparent, and technology-driven manner. The Board strives to encourage voluntary compliance, protect the rights of honest taxpayers, facilitate trade with risk-based enforcement, and enable the legitimate movement of people, goods, and services.

Role and Functions of the Central Board of Indirect Taxes and Customs (CBIT&C)

The Central Board of Indirect Taxes and Customs (CBIT&C) is responsible for various important functions related to the collection and regulation of indirect taxes in India. Here are the key roles and functions of the CBIT&C:

- Collection of Taxes: The CBIT&C is responsible for collecting Goods and Services Tax (GST) and customs duties from various locations, including international airports, seaports, inland container depots, special economic zones (SEZs), and container freight stations.

- Prevention of Smuggling: The board plays a crucial role in preventing smuggling activities at international airports, seaports, and through land customs stations and border checkpoints.

- Communication: The CBIT&C is responsible for acknowledging all written or electronic communications, such as declarations, intimations, applications, and returns. It also communicates its decisions regarding these matters.

- Refunds: The board handles refund claims related to customs duty and GST.

- Drawbacks: Drawbacks in duty are sanctioned in cases of claims or the fixation of brand rates of duty.

- Cargo Release: The CBIT&C determines the release time for cargo in export cases for sea cargo, air cargo, inland container depots, and land customs stations. For imports, it decides the release time for all these modes of transport.

- GST Facilitation: The board facilitates GST registration, amendments, and cancellations when eligible.

- Audit: The CBIT&C informs in advance when it undertakes a GST or customs audit and communicates the results of the audit once it is completed.

Conclusion

A robust tax administration system is crucial for guiding the economy towards growth and development. It should adhere to the principles of effective taxation, such as setting the right tax percentage relative to the Gross Domestic Product (GDP) to minimize tax evasion and avoidance.

- The taxation policy needs to be simple and transparent to foster taxpayer confidence, except in cases where certain practices, like the sale of alcohol or cigarettes, need to be promoted or discouraged.

- Implementing progressive taxes is essential to enable taxpayers to compete globally while ensuring efficient tax collection to provide necessary infrastructure.

- Additionally, governments should encourage investments in cleaner technologies across various industries by offering tax reductions to taxpayers who invest in environmentally friendly practices.

- There are ongoing global initiatives aimed at creating a low-carbon economy, and organizations like the Association of Chartered Certified Accountants (ACCA) believe that taxation is a dynamic economic and social tool that should evolve as national economies and business landscapes change.

|

19 videos|83 docs|14 tests

|

FAQs on Types of Taxes - Goods and Services Tax (GST) - B Com

| 1. What are direct taxes at the central level? |  |

| 2. Which taxes are classified as indirect taxes levied by the state government? | |

| 3. What are the features of direct taxes? | |

| 4. What are the merits of direct taxes? | |

| 5. What are the demerits of direct taxes? | |

past year papers

,Types of Taxes | Goods and Services Tax (GST) - B Com

,Exam

,Previous Year Questions with Solutions

,ppt

,MCQs

,Sample Paper

,study material

,Summary

,Types of Taxes | Goods and Services Tax (GST) - B Com

,mock tests for examination

,Free

,Types of Taxes | Goods and Services Tax (GST) - B Com

,video lectures

,Viva Questions

,shortcuts and tricks

,Extra Questions

,practice quizzes

,Objective type Questions

,Important questions

,Semester Notes

;

Types of Taxes Free PDF Download

Importance of Types of Taxes

Types of Taxes Notes

Types of Taxes B Com Questions

Study Types of Taxes on the App

|

© EduRev

|

Education Revolution

|

|