Cheat Sheet: Municipality | Indian Polity for UPSC CSE PDF Download

Introduction

This chapter explains how urban areas in India are governed by elected local bodies to manage cities and towns effectively. It covers the types of urban local governments, their historical development, the 74th Constitutional Amendment Act of 1992, municipal personnel, revenue sources, and the role of the Central Council of Local Government. The goal is to show how these systems ensure better urban administration and local democracy.

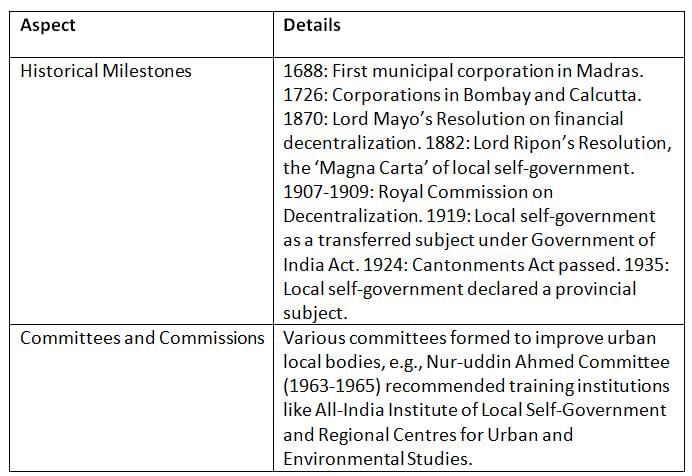

Evolution of Urban Local Government

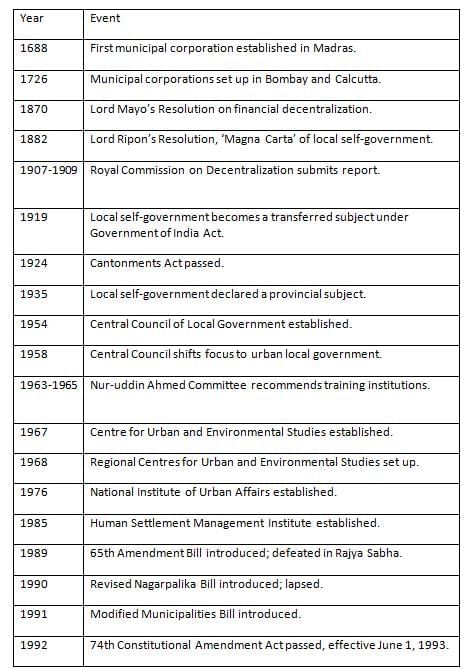

Urban local government in India began during British rule and evolved through key resolutions and acts. It became a formal part of the Constitution with the 74th Amendment in 1992, aiming to strengthen urban governance.

Key Points: Urban local government evolved from British-era corporations to a constitutionally recognized system, with key resolutions and committees shaping its growth.

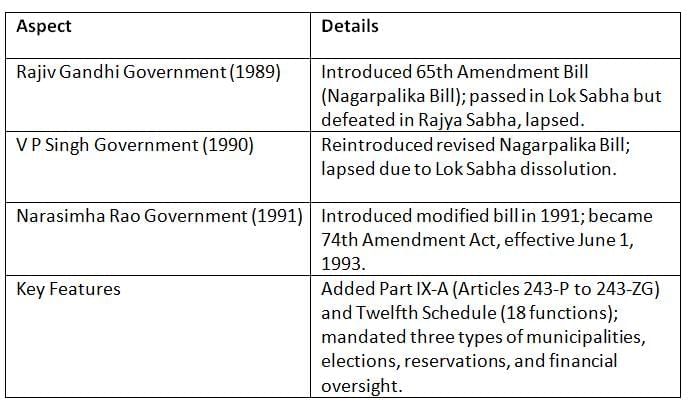

Constitutionalization of Urban Local Government

Efforts to give urban local bodies constitutional status began in 1989 but faced setbacks. The 74th Amendment Act of 1992 successfully formalized municipalities, ensuring their role in urban governance.

Key Points: The 74th Amendment gave municipalities constitutional status, ensuring a uniform structure and empowering urban governance.

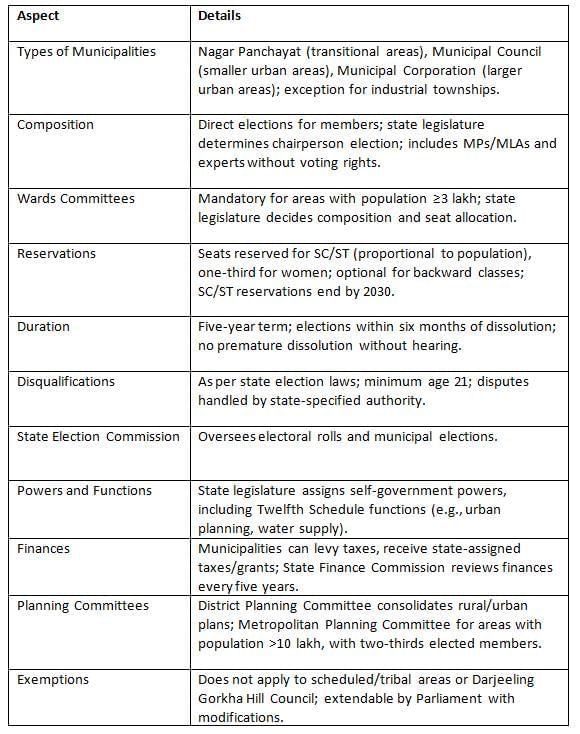

74th Constitutional Amendment Act of 1992

The 74th Amendment Act introduced a structured system for urban local governance, defining municipalities’ roles, composition, and powers to promote effective self-government.

Key Points: The 74th Amendment ensures municipalities have defined structures, elections, reservations, and financial powers, with planning committees for coordinated development.

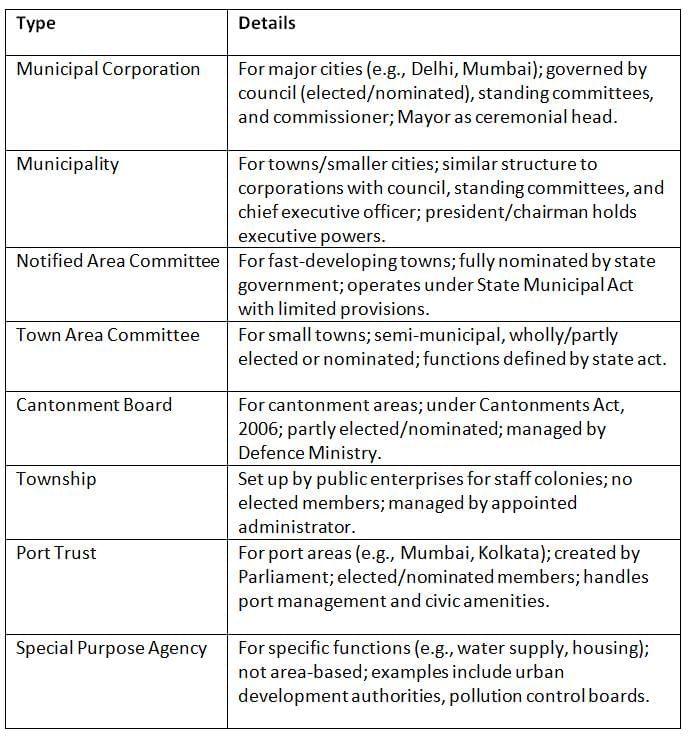

Types of Urban Local Government

India has eight types of urban local bodies, each designed to manage specific urban areas or functions, ensuring tailored governance for diverse urban needs.

Key Points: The eight types of urban local bodies cater to diverse urban areas, from large cities to specialized functions, ensuring effective local governance.

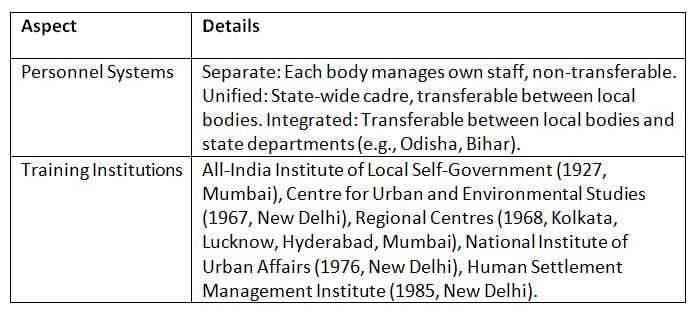

Municipal Personnel

Municipal personnel systems manage staff for urban local bodies, varying by state, with training institutions supporting capacity building.

Key Points: Municipal personnel systems vary by state, with national training institutions enhancing skills for effective urban governance.

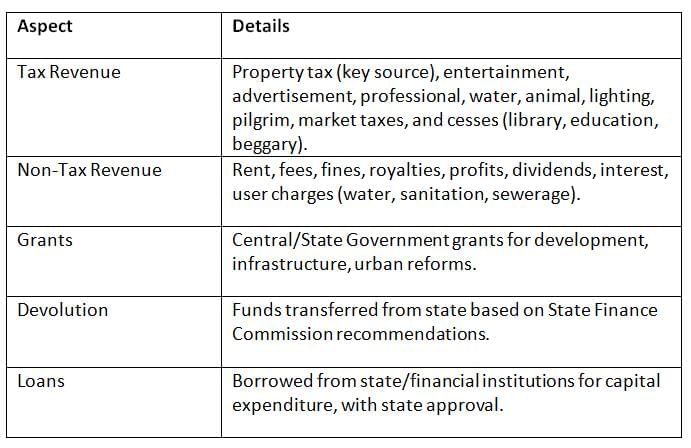

Municipal Revenue

Urban local bodies rely on diverse revenue sources to fund their operations, but face challenges in achieving financial independence.

Key Points: Municipalities depend on taxes, grants, and loans, with property tax being the most significant revenue source, but face constraints due to limited fiscal autonomy.

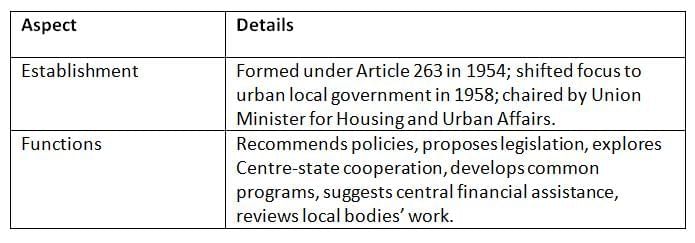

Central Council of Local Government

Established in 1954, the Central Council of Local Government advises on urban local governance, focusing on policy, legislation, and financial assistance.

Key Points: The Central Council supports urban local governance by guiding policy and financial aid, fostering coordination between Centre and states.

Chronology for Quick Revision

Conclusion

This chapter highlights how urban local government in India ensures effective city and town management through elected bodies. The 74th Amendment Act formalized municipalities, defining their structure, powers, and finances. Various urban bodies, from corporations to special agencies, address diverse urban needs, supported by personnel systems and revenue sources. The Central Council of Local Government aids policy and coordination. Despite progress, challenges like limited fiscal autonomy persist. Strengthening these systems is vital for vibrant urban democracy and sustainable development.

|

154 videos|989 docs|260 tests

|

FAQs on Cheat Sheet: Municipality - Indian Polity for UPSC CSE

| 1. What is the significance of the 74th Constitutional Amendment Act of 1992 in the context of Urban Local Government in India? |  |

| 2. What are the different types of Urban Local Governments recognized in India? | |

| 3. How is municipal revenue generated and what are the primary sources? | |

| 4. What role does the Central Council of Local Government play in urban governance? | |

| 5. What are the key responsibilities of municipal personnel in Urban Local Governments? | |

past year papers

,video lectures

,study material

,Summary

,Important questions

,shortcuts and tricks

,Viva Questions

,Extra Questions

,ppt

,Free

,mock tests for examination

,practice quizzes

,Sample Paper

,Cheat Sheet: Municipality | Indian Polity for UPSC CSE

,Exam

,Previous Year Questions with Solutions

,Cheat Sheet: Municipality | Indian Polity for UPSC CSE

,Objective type Questions

,MCQs

,Semester Notes

,Cheat Sheet: Municipality | Indian Polity for UPSC CSE

;

Cheat Sheet: Municipality Free PDF Download

Importance of Cheat Sheet: Municipality

Cheat Sheet: Municipality Notes

Cheat Sheet: Municipality UPSC Questions

Study Cheat Sheet: Municipality on the App

|

© EduRev

|

Education Revolution

|

|

within 7 days!